The balanced scorecard (BSC) is a widely used performance measurement framework for strategic planning. It is so popular, in fact, that The KPI Institute’s latest State of Strategy Management Practice report found that 40% of respondents from Middle Eastern companies were using it. Why is that the case? It’s likely in the name—the BSC offers a balanced perspective of a company’s performance, focusing not just on financial gains but the various aspects of value creation as well. This enables companies who use it to establish sustainable business practices that can meet long-term goals without sacrificing short-term improvements.

What Is the BSC?

In 1992, Robert Kaplan and David Norton dreamed of a better way. Aware of the limitations of traditional practices that focused solely on financial indicators such as return on investment (ROI) to measure a company’s performance, the two designed a tool that incorporated non-financial variables to paint a more holistic, comprehensive picture. Thus, the balanced scorecard was born.

The BSC was further refined by connecting performance metrics directly to strategy, which marked a formal link between strategic goals and performance measurement. In 1996, it became a performance management system (PMS) that effectively integrated the various crucial aspects of an organization—i.e. strategic processes, resource allocation, budgeting and planning, goal setting, and employee learning.

By 2001, the BSC had outgrown its original form, no longer seen as a mere management tool but instead as an all-encompassing strategic management and control system. The BSC has continued to evolve alongside the ever-changing priorities of the business world. In 2021, many companies began integrating environmental and social dimensions into their BSCs to reflect their triple bottom line strategies.

The BSC gives managers a view of the business from four crucial perspectives. Each perspective deals with an integral aspect of the organization and answers a specific question:

Customer Perspective: How Do Customers See Us?

Companies typically have a mission statement that encapsulates how they interact with customers. For example, e-commerce platform Etsy’s mission statement is “Keep Commerce Human.” This sentiment informs the way the company does business, which places importance on leaving a positive economic, social, and ecological impact.

The BSC holds companies accountable to their mission statements by translating them into specific measures that must be followed. For Etsy, one aspect to consider would be the diversity of its workforce, which falls under social impact. To address this, the company has taken measures such as increasing the presence of underrepresented communities in its seller community by interviewing candidates from those backgrounds. This has enabled the company to stay true to its mission and show customers that it walks the talk.

Internal Perspective: What Must We Excel At?

Balance is the primary focus of the BSC—it’s in the name, after all. Thus, the framework doesn’t only take into account the way customers perceive the company, but it also considers what the latter does to shape this perception. This is composed of the various operational and organizational processes that drive the company.

By giving managers an internal perspective, they can identify, track, and measure the processes that yield the most benefits and close the gaps on the ones that fall short.

Learning and Growth Perspective: Can We Continue to Improve and Create Value?

The business landscape is constantly shifting, and in order to keep pace with its changes, businesses must consistently learn and innovate. That is the importance of this perspective, which states that a company’s value hinges on its ability to improve. In any industry, competition can be fierce, which means companies must always find new ways to stand out.

Financial Perspective: How Do We Look to Shareholders?

Among the four perspectives, this is perhaps the most straightforward. Put simply, it indicates if a company is profitable. Although financial performance is no longer the end-all, be-all measure of a company’s success, it still plays a crucial role in determining whether a company is simply surviving or thriving. Shareholders understandably value profitability, and they won’t keep investing in a company that doesn’t produce ROI.

The BSC is by nature a holistic framework, meaning each part is interconnected to the others. This is why it’s important to take a balanced (pun intended) approach when considering the four perspectives. If one side is prioritized over the others, it could lead to the formation or widening of inefficiency gaps that impede business growth and success.

As previously mentioned, the BSC is quite popular. This is due to the myriad of benefits that it brings to organizations that use it wisely. The most obvious benefits of the BSC are twofold. First, it consolidates the seemingly disparate aspects of a business in a single report, leading to increased efficiency in performance reporting and measurement as well as faster decision-making. Second, the BSC helps mitigate suboptimization by making managers consider the entirety of the company’s operational measures, demonstrating whether one objective was achieved at the cost of another.

A more concrete example of the BSC benefiting companies can be seen in how Apple uses the framework. By shifting its focus from innovating its products to also paying mind to customer satisfaction by establishing it as one of the company’s core tenets, the tech giant was able to improve its already stellar reputation by catering to its customers’ desires. Apple also values core competencies, employee commitment and alignment, market share, and shareholder value. Together, these indicators make up the metrics of their BSC.

World-renowned electronic company Philips is also known for its use of the BSC, using a bespoke version of the framework to fit its organizational needs. The company’s focus is on its employees, and it uses the BSC to ensure that each member of its workforce has a clear understanding of the company’s strategic policies and long-term vision.

What Does the Future Hold?

There must be a stronger emphasis on customization as companies realize that there is no such thing as a one-size-fits-all approach to performance management. This aligns with the proliferation of new advancements in artificial intelligence (AI) and machine learning (ML), technologies that must be integrated into the BSC lest the framework fall behind the ever-shifting realities of the business world. Regardless of the future, the BSC appears poised to remain a vital tool for companies of all sizes and in all industries.

Interested in learning more about the BSC? Browse our articles here.

In an era when environmental concerns are at the forefront of global discussions, businesses are being called upon to integrate sustainability into their operations. Developed as an extension of the traditional Balanced Scorecard (BSC), the Sustainability Balanced Scorecard (SBSC) aims to provide businesses with a tool to align their environmental, social, and economic objectives, driving positive impact while ensuring long-term success.

The genesis of the SBSC

The concept of the BSC was first introduced by Robert Kaplan and David Norton in the early 1990s as a framework to measure business performance beyond financial metrics. The BSC aimed to provide a more holistic view of an organization’s health by incorporating four hierarchical perspectives: Financial, Customer, Internal Processes, and Learning & Growth.

A decade later, as sustainability became a critical global concern, scholars started looking into the possibility of integrating sustainability considerations into the BSC. They agreed on the potential of extending the focus of the well-established BSC to include measuring business performance through the lens of environmental stewardship, social responsibility, and ethics. Thus, the concept of the SBSC began to crystallize .

How to build an SBSC

When it comes to the best architecture for the SBSC, there have been conflicting discussions ever since the concept was introduced. Two major approaches took prominence: one is to add a fifth perspective to the traditional BSC that was dedicated to sustainability; the other is to integrate sustainability objectives and KPIs into the already existing perspectives.

A 2009 study showed that in the fifth perspective approach, sustainability KPIs tend to be overlooked by management in organizations with no established sustainability culture. That is why the four-perspective approach can be a safer choice, especially for organizations that are only starting to integrate sustainability in their measures.

In a 2021 article, Kaplan supported the four-perspective approach, introducing a suggested restructuring of three out of the four perspectives to make them more relevant to environmental, social, and governance (ESG) elements:

From “Financial” to “Outcomes” to include environmental and societal objectives besides the financial aspect

From “Customer” to “Stakeholder” to reflect the value of different members of the whole ecosystem

From “Learning & Growth” to “Enablers” to encompass the various capabilities across all stakeholders in the ecosystem

Reaping these sustainability integration benefits can be a bit of a long shot, and further studies are needed to prove such benefits even exist. However, the only way to reap said benefits is to plant the seeds of sustainability integration. To help accomplish this, the SBSC can be a potent tool that allows organizations to measure, manage, and optimize their sustainability performance. As global challenges such as climate change, resource depletion, and social inequality loom larger, businesses must go beyond profits and consider their broader impact. The SBSC empowers organizations to embrace sustainability as a strategic imperative, paving the way for a more responsible, resilient, and prosperous future.

For more on utilizing the Balanced Scorecard, The KPI Institute has developed the Certified Balanced Scorecard Management System Professional to help organizations maximize the tools’ potential. And if you are interested in expanding your toolkit further, consider subscribing to smartkpis.com and gain access to the world’s largest database of documented KPIs, which includes a thorough collection of sustainability metrics.

Often than not, several executives take strategy as a routine task or a series of frameworks instead of a mode of visualizing and solving problems. Furthermore, taking on the newest strategy trends or following a successful entrepreneur’s guidelines is not an ideal way to win. Companies need to take their strategies through a series of tests to determine their validity.

There are three tests that identify the success of strategies. These assessments help executive teams to answer some of their burning question, such as:

a) Does your company strategy respond to uncertainty and trends?

b) Does your strategy exploit legitimate sources of advantage?

c) Is your strategy aligned and cascaded throughout your organization?

Three Winning Strategy Tests

There are three types of tests companies can apply to determine whether their strategies are viable or not. The first one is the Fit Test. This type of test measures the level of fitness of a company’s strategy along with its business condition. When conducting the Fit Test, there are three fit dimensions that need to be assessed: internal fit, external fit, and dynamic fit.

Internal fit and external fitare the keys to securing a company’s survival (Tyge Payne et al., 2015). Internal fit is described as a multi-dimensional matching of strategy with structure. It is undertaken to ensure that the strategy matches the company’s resources as well as competitive capabilities. Winning strategies display an internal fit and must be compatible with the ability of a company to implement the strategy in a competent mode.

External fit refers to the congruence between an entity’s strategy and composition and its task environment. Testing external fit will exhibit how a strategy matches significantly with the external conditions, such as industry dynamics, competition, and market opportunities. Therefore, a strategy will only work well if it has an excellent external fit against the external environment.

The last type of fit test is dynamic fit. It is a fundamental measurement that assesses if strategies are changing over time. Dynamic fit is used to synchronize and align the current state of the business with market conditions.

According to Jonathan Trevor and Barry Varcoe, retaining a good strategic alignment relies on the ability of a company’s structure, procedures, and culture to evolve with strategy changes. The signs of misalignments are always evident to employees and customers who fail to receive the type of service they expect.

The second type of test is called the Competitive Advantage Test. This type of test measures the lasting competitive advantages of businesses in the market space. The Competitive Advantage Test also enlightens managers on strategies that often fail to keep up a constant competitive advantage with rivals. Failed approaches to maintain a competitive advantage over competitors usually lead to inferior performance in the long run.

As winning strategies enable competitive advantage to be durable and larger, the research of competitive advantages in the tech industry by (Huang et al., 2015) sheds light on the outcome differences between Temporary Competitive Advantage (TCA) and Sustainable Competitive Advantage (SCA).

The paper suggests that companies can achieve higher outcomes through SCA by amassing assets, resources, and capabilities. However, TCA created through strengthening market positions can assist firms with capital to accumulate resources that will develop a sustainable competitive advantage.

The Performance Test is the third form of measurement to differentiate a winning or losing strategy. A performance test is vital for organizations as companies usually mark their success based on performance. There are two types of indicators that a company looks at to understand the standard of this strategy test:

a) Competitive strength and market positioning and

b) Profitability and financial strength.

One of the performance measurements tools that businesses can use to effectively manage organizational performance is the balanced scorecard. It provides a holistic strategy implementation framework comprising five elements: desired state of evolution, strategy map, performance scorecard, performance dashboard, and portfolio of initiatives.

To sum it up, a company’s strategy needs to excel in all tests to succeed. Failing in even one of the tests could spell problems for business ventures and lead to negative performance. A company can introduce new practices only if they match or erase both internal and external conditions. On the other side, existing strategies should always be evaluated thoroughly to affirm that they are fit and contribute to good performances and competitive advantage. Incorporate fast changes to current strategies if companies fail at least one of the three tests.

Take a look at The KPI Institute’s website and find out more about the Certified Balanced Scorecard Management System Professional course. Discover new approaches on how to create a performance management system based on the balanced scorecard technique and how to implement it at all levels of the organization.

The world is moving towards a more sustainable business practice. Investors, advocacy groups, and academics have asked corporations to take on added purpose beyond the traditional pursuit of shareholder value. Even the business leaders from Business Roundtable stated that major companies are investing in their employees and communities because they realize it is the only way to achieve long-term success.

The fundamental concept behind this shift is the Triple Bottom Line (TBL), where companies must measure not only their financial performance but also their environmental and societal performance as well. The TBL concept is not new; the term had been coined by John Elkington in the 1990s. Later in 2003, Amanco pioneered in measuring the impact of its TBL strategy, building on the idea of Balanced Scorecard (BSC) from Kaplan and Norton. The new sustainability BSC included environmental and social dimensions in addition to the basic dimensions of the initial BSC.

In a recent article, Kaplan stated that the demands for sustainability today are even higher. In summary, there are three different perspectives from three main stakeholders categories:

Customers: The customers’ preferences in every product category shifted towards more sustainable products. Over the past five years, there is a 71% rise in online searches for sustainable goods globally in countries with either developed or emerging economies.

Employee: Reports of unsafe working conditions at Amazon warehouses caused many criticisms. Their employees protested for fair pay and COVID protection. This example reflects the importance of social and ethical issues. Fulfilled workers are more loyal and likely to stay compared to those who only work for a weekly paycheck. Worse, incidents like this would probably affect consumers’ perception badly and hurt the company’s brand image.

Environment and social: As more consumers demand transparency and accountability, companies must consider the environmental and social aspects in every decision they make. For example, major fashion brands are beginning to pay attention to the demand for more sustainable practices.

The stakeholders have always played an important role in the business ecosystem. But in today’s post-pandemic era, the stakeholders expect even more from companies in terms of environment (e.g., sustainability, health) and social (e.g., inclusive, ethics, social welfare) aspects. As with any crisis, there are chances to learn and make a positive difference.

This article aims to remind companies of the criticality of environment and social dimensions. Taking note of its importance, this might be the opportunity to revisit the idea of sustainability BSC. The sustainability BSC can be used as a groundwork for a future BSC that is environmentally, socially, and ethically responsible. For more on utilizing the Balanced Scorecard, The KPI Institute has developed the Certified Balanced Scorecard Management System Professional to help organizations maximize the tools’ potential.

Throughout the years, many studies have examined the use of the balanced scorecard (BSC) in a board’s performance evaluation. Why is this important and how can this be implemented?

The modern business landscape is characterized by fast-changing trends, an expanding weight from the competition, and risks emerging from new trends. This is why a good corporate governance system is what can help companies achieve high business performance despite uncertainties. Having a control mechanism will help managers carry out business activities that can maximize profits for shareholders. Board members represent an important internal control mechanism.

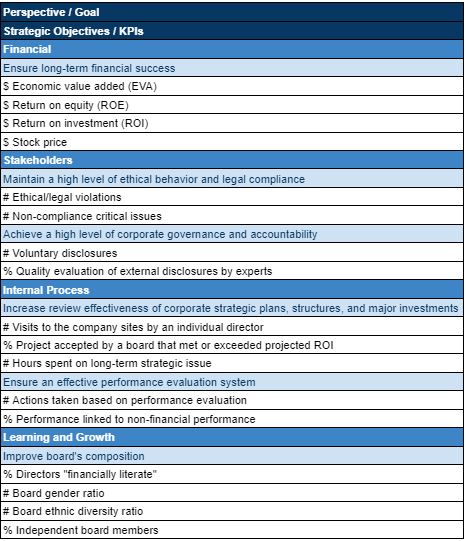

BSC, designed by Robert Kaplan and David Norton, is primarily made of financial and non-financial benchmarks. The BSC model starts from a defined mission, vision, goals, and strategy of the company and identifies specific goals, tasks, benchmarks, and initiatives from four basic causal relationships: financial perspective, stakeholder perspective, internal business process perspective, and learning-growth perspective.

The BSC component in a board’s performance context

In 1996, Kaplan & Norton suggested that the vision and strategy of a company be more specifically defined from four basic, interconnected perspectives:

Financial Perspective – how to implement a strategy that will maximize profits for equity owners.

Customer Perspective – how to achieve customer satisfaction and loyalty.

Internal business process – how to achieve an effective and efficient business process.

Learning and Growth Perspective – how to gain human capital competitive advantage.

Later, in 2004, Kaplan & Michael E. Nagel proposed a three-part BSC program:

Enterprise Scorecard – synchronized list of results at company level

Board Scorecard – synchronized list of Board results

Executive Scorecard – synchronized list of executors’ scores

Synchronized lists at the company level ensure that top managers, starting from a well-defined company strategy, goals, tasks, benchmarks and initiatives through the four outlined perspectives. This process converts the company’s strategy into operational terms.

It is necessary to build a synchronized list at the board level. That is, the board of directors should evaluate and approve the corporate strategy map and the corporate level’s harmonized list. According to Kaplan and Nagel, a synchronized list at the board level also has four perspectives:

Financial Perspective – Similar to the company level, the goal is to maximize value for equity owners.

Stakeholder perspective – This is a broader perspective than at the company level because it is now important to respect the interests of all stakeholders.

Perspective on internal business processes – This explains how the board contributes to achieving shareholder goals and relates to performance monitoring, reward systems, etc.

Learning and Growth Perspective – This captures human capital as a source of competitive advantage, related to the specific skills and the knowledge and capabilities of board members.

Application of the BSC to a board’s performance evaluation

According to research published in the Managerial Auditing Journal, studies that have suggested the possibility of using the BSC in evaluating the board performance recognize the financial dimension, the stakeholders’ dimension, the internal processes dimension, and the learning and growth dimension in the BSC.

The framework of the board’s BSC is based on identifying four basic elements in each dimension: the objectives, the performance drivers, the measures, and the targets:

The objectives reflect the board responsibilities;

The performance drivers are actions taken by the board to achieve the objectives. Each performance driver should be linked to specific measures and targets;

The performance measures are used to control the performance drivers and assess whether the board has achieved the goals;

The targets reflect the best practices of the industry.

Using BSC in a board’s performance evaluation can help define strategic contributions of the board; provide a tool to manage the composition and the performance of the board and its committees; clarify the strategic information required by the board, and help monitor the structure and performance of the board and its committees.

The evaluation process: agents and contents

According to the study “Evaluating Boards and Directors”, evaluating board performance may be done by an internal party represented by the chairman of the board. In some cases, it may be appropriate to delegate the evaluation process to a non-executive member, a lead director, or a committee of the board. Also, the evaluation process may be carried out by an external party who has experience in corporate governance and performance evaluation.

The self-evaluation method is a common way to evaluate board performance. Even though this method is characterized by confidentiality, biases can still occur. The close work relationship between chairman or the non-executive member and the board members can affect the objectivity of their point-of-view. The lack of skills and time in conducting performance evaluation can be a major influence on the evaluation results.

Through a nominating committee or an audit committee, a higher degree of objectivity and independence can be achieved; however, the bias risk will remain.

Hiring an external advisor is applicable for the non-availability of the necessary skills for the evaluation process and achieving greater transparency and objectivity. The external counselor may be a professional advisor. Several enterprises use a trusted adviser as the board prefers to deal with people whom they know and trust, but it is better to use a professional advisor that has a proven technical skill in their past experiences and a high degree of independence.

– The responsibilities element aims to evaluate the fulfillment of the board’s responsibilities.

– The operations element aims to assess the board’s relationship with the management.

– The structure element aims to assess the board’s composition.

– The board membership element aims to assess the overall board’s skills and knowledge, experience, competence, ethics, diligence, and independence.

Image source: The KPI Institute

The BSC is an advanced performance management tool that supports organizations to transform vision and strategy into short-term and long-term targets and specific measuring rules. The application of a balanced scorecard in evaluating a board’s performance has been proven through many studies as an effective performance management tool. It also helps a board’s direction to be more aligned at the company and operational level.

Using a BSC in a board’s performance evaluation requires skillful and independent evaluation agents to maximize its potential. To gain the right skills and learn how to implement a balanced scorecard management system in your organization, sign up for The KPI Institute’s Certified Balanced Scorecard Management System Professional course.