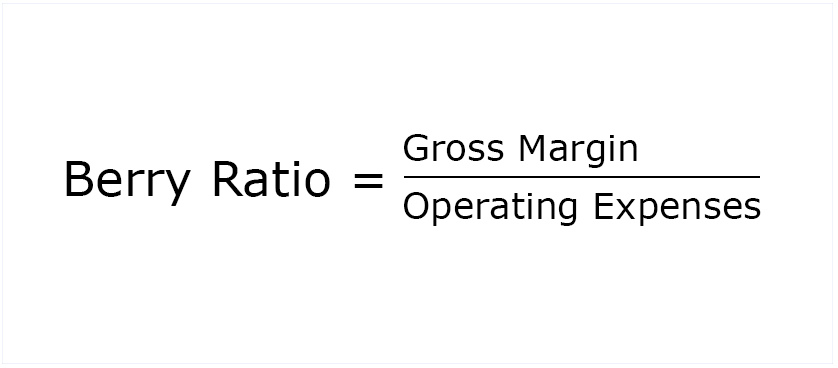

Measuring company profitability with the Berry ratio

Companies use profitability ratios in order to measures their ability to generate returns through effective allocation and use of available resources. KPIs in this area have often as main component profit or return. One of the most popular profitability ratios is the Berry ratio.